Where is healthcare today and what role can startups play? A story in 10 pictures

[ad_1]

At Tau Ventures we invest in AI in digital health and AI in enterprise. If a picture is worth a thousand words, this article will attempt telling a story in 10 pictures.

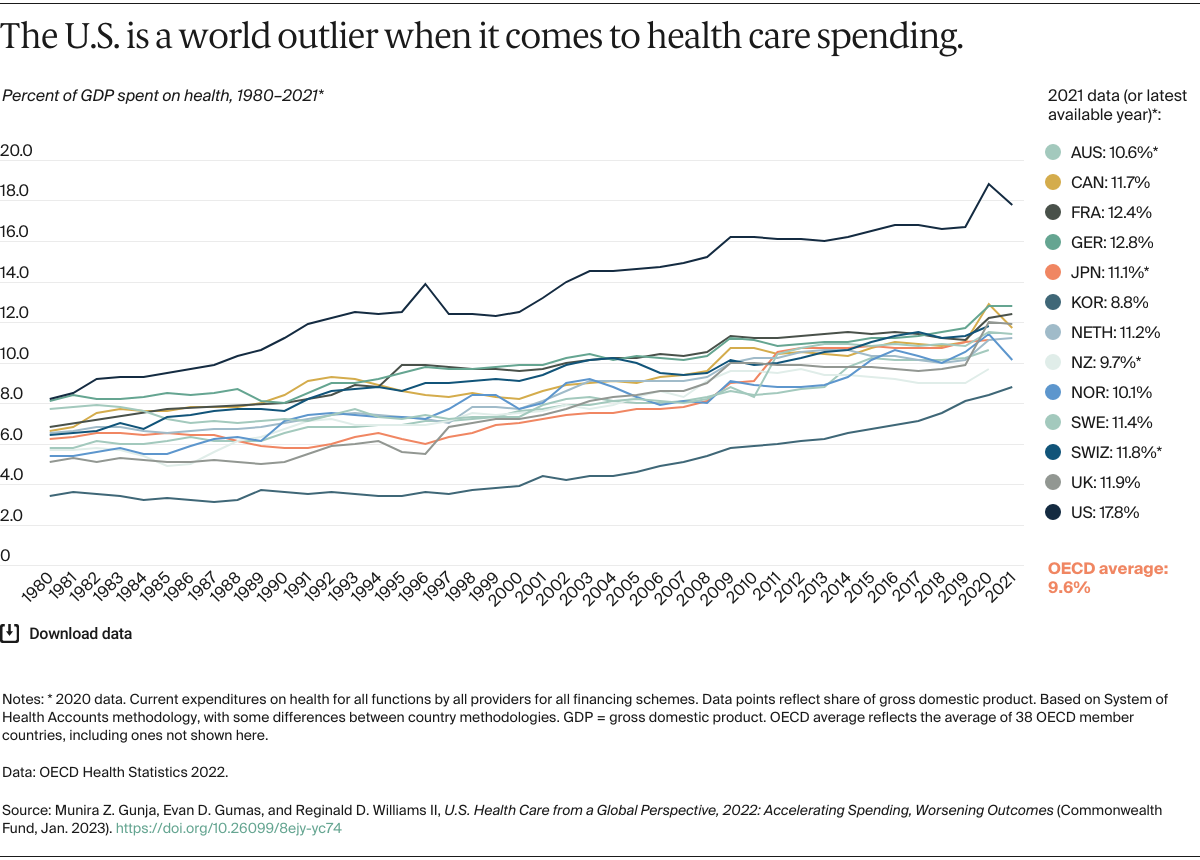

Figure 1

In 1980 the US was still in line with other developed countries when it comes to healthcare expenditure. Since then we have increased this expenditure much faster than any other of these peers. In fact, in 2021 our spend was essentially double relative to the average for OECD (Organisation for Economic Co-operation and Development) which aggregates mostly high-income countries. Is it because of worsening dietary habits including cheaper, more processed food? Is it because of higher stress? Is it because of less exercise? Is it because of institutional misalignments where we pay increasingly more to get increasingly less healthcare? There are many explanations but the fact is our healthcare is increasingly unsustainable.

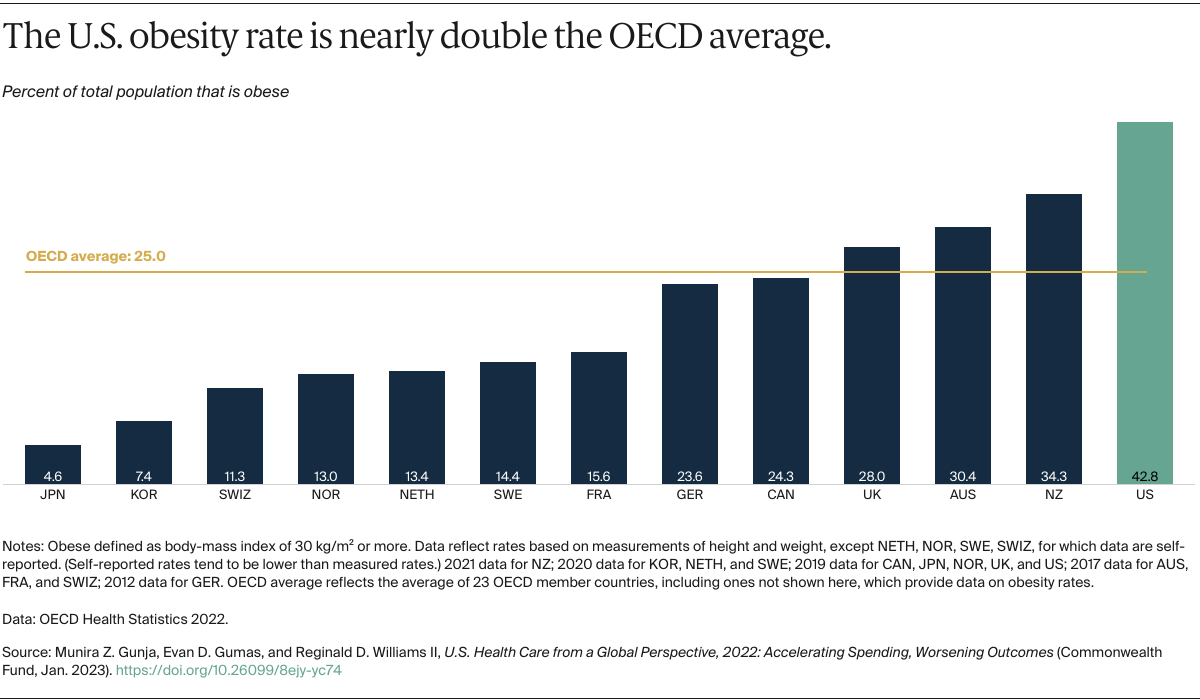

Figure 2

Obesity is the canary in the coal mine given it causes or exacerbates many other health problems. And it’s truly a national emergency in the US. Other developed countries don’t have nearly the same levels, although they are also facing surges. The biggest new challenge is arguably developing countries, which have skyrocketed in obesity in a matter of a generation as most of the world has moved from scarcity to plenty.

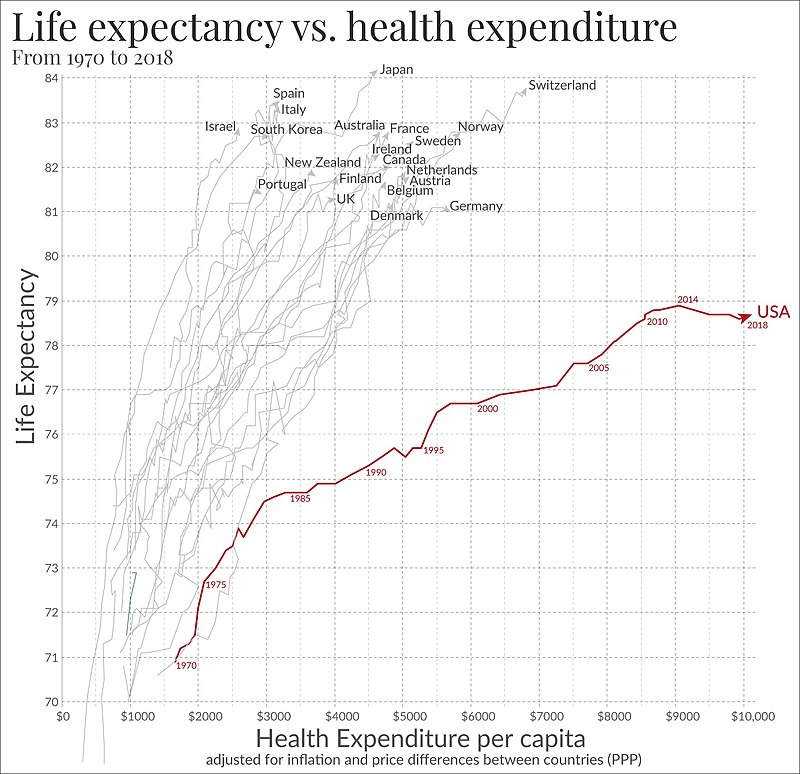

Figure 3

In many ways this figure summarizes the previous two. We are basically spending ever more in healthcare but not getting better results. In fact, even before the COVID pandemic, the US was already seeing a decline in life expectancy. What are we doing wrong?

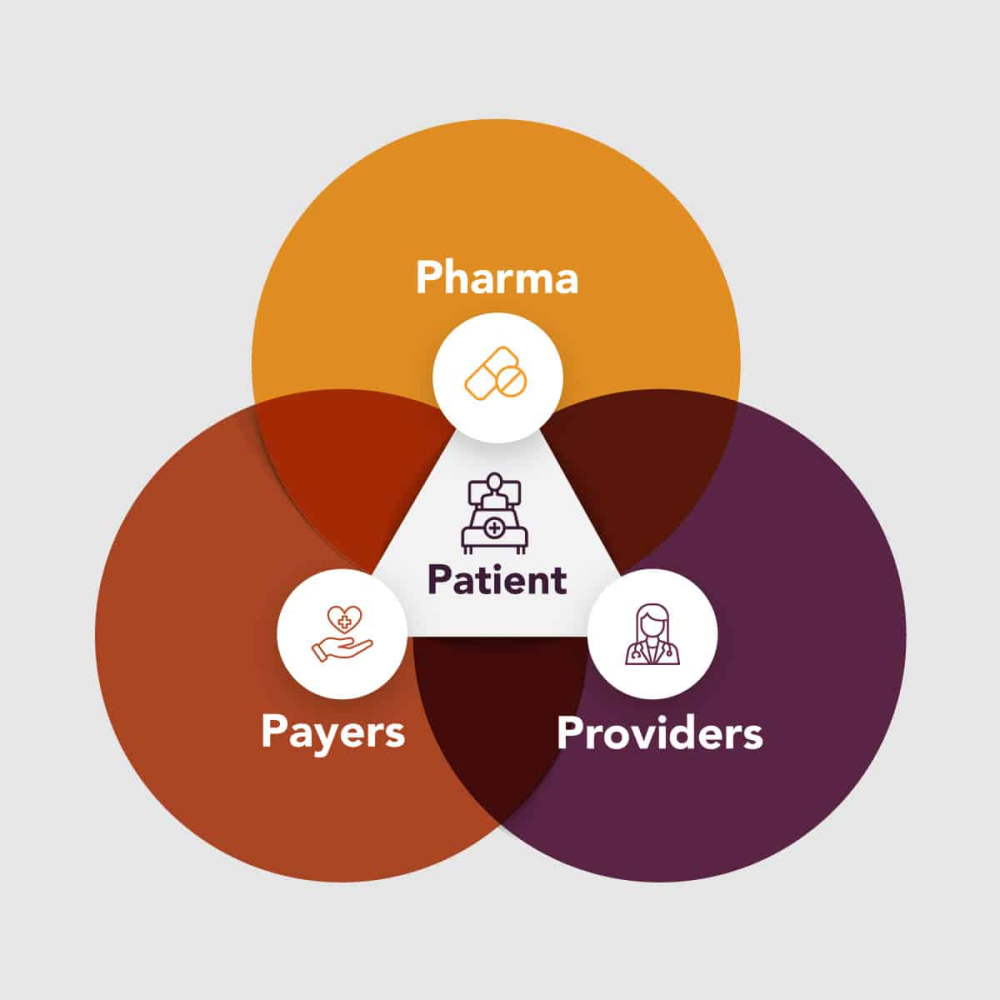

Figure 4

The traditional view of healthcare is the 4Ps: patients, providers, payors, pharma. Many would add a fifth, policymakers. Understanding the interplay of these different stakeholders has been key to deciphering the challenges and opportunities in healthcare. As our models and metrics evolve, so have our business models. Fee per service has been supplanted by capitation payments which is being supplanted by value-based care. Big Tech is increasingly making foray into healthcare, Big Health is responding by buying / building / partnering with digital health. Startups, increasingly powered by AI, are flourishing now that there is more data, more computational power, and increasingly more need.

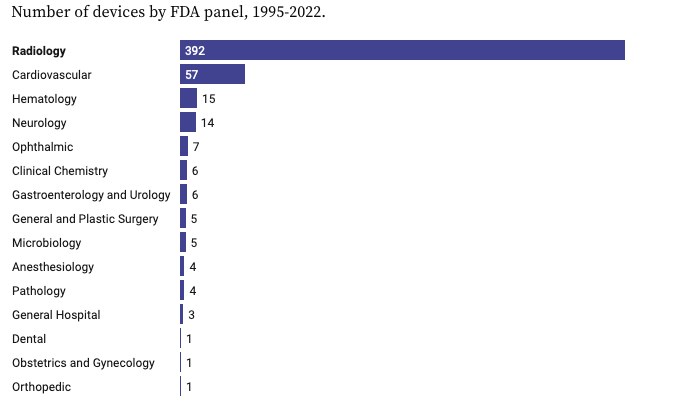

Figure 5

A big factor also making it easier for healthcare startups to blossom are regulatory frameworks. Radiology unsurprisingly leads the pack – imaging is its core and understanding what story images tell is something software can increasingly do better. But the other areas of medicine are also growing, at Tau Ventures we are especially interested in this next wave.

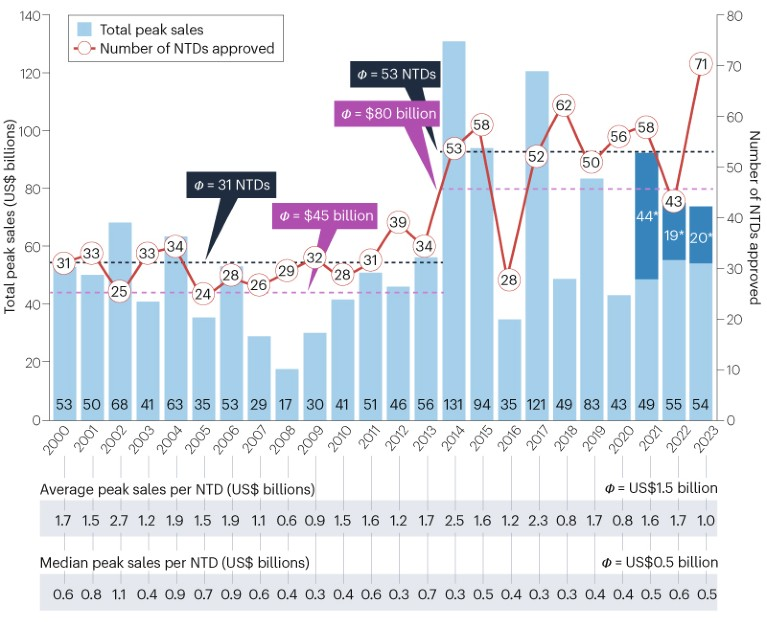

Figure 6

Making drugs has historically been a very expensive and time-consuming process. But software helping with the analysis and development has been a major factor for flattening the world a little. More new therapeutic drugs were approved in 2023 than ever before. Their more moderate sales are a suggestion that the business model is shifting a bit. Maybe a company doesn’t necessarily need a blockbuster but can actually be profitable enough by making and selling drugs cheaper. Maybe that ushers us closer to true personalized medicine. Maybe these are fruits of our garage moment i.e. it’s possible to build successful life sciences companies with fewer resources.

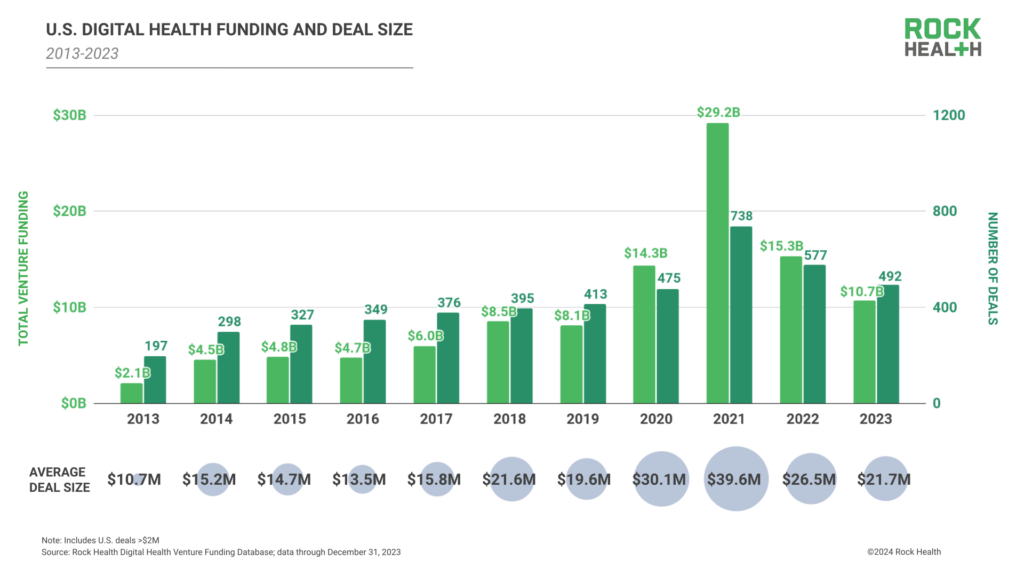

Figure 7

The funding for healthtech has been growing steadily, actually at a higher pace than the average for venture capital. The COVID years saw a big jump in many industries and then a precipitous decline. But 2023 ended essentially as a continuation of 2019, the last full year before COVID, which may be an indication for what the future holds. If interest rates do come down as expected in 2024, it will be a boon for startup activity.

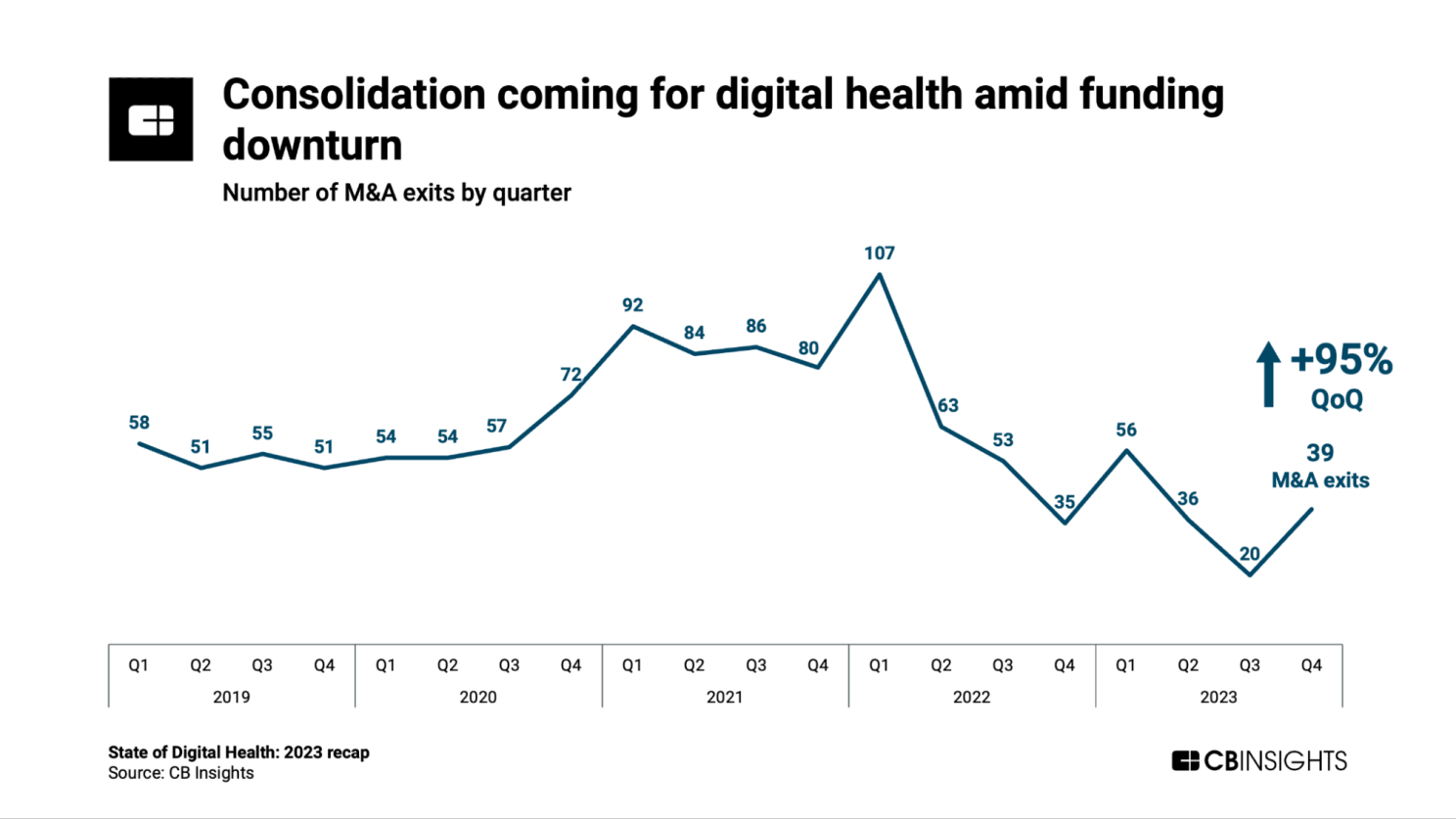

Figure 8

The previous figure shows a higher number of smaller deals, many of them at an earlier stage. If there is less money relatively speaking for later-stage companies then there will invariably be a bigger pressure for consolidation. Our view at Tau Ventures is indeed a significant uptick in M&A in 2024 before there is a recovery in IPOs.

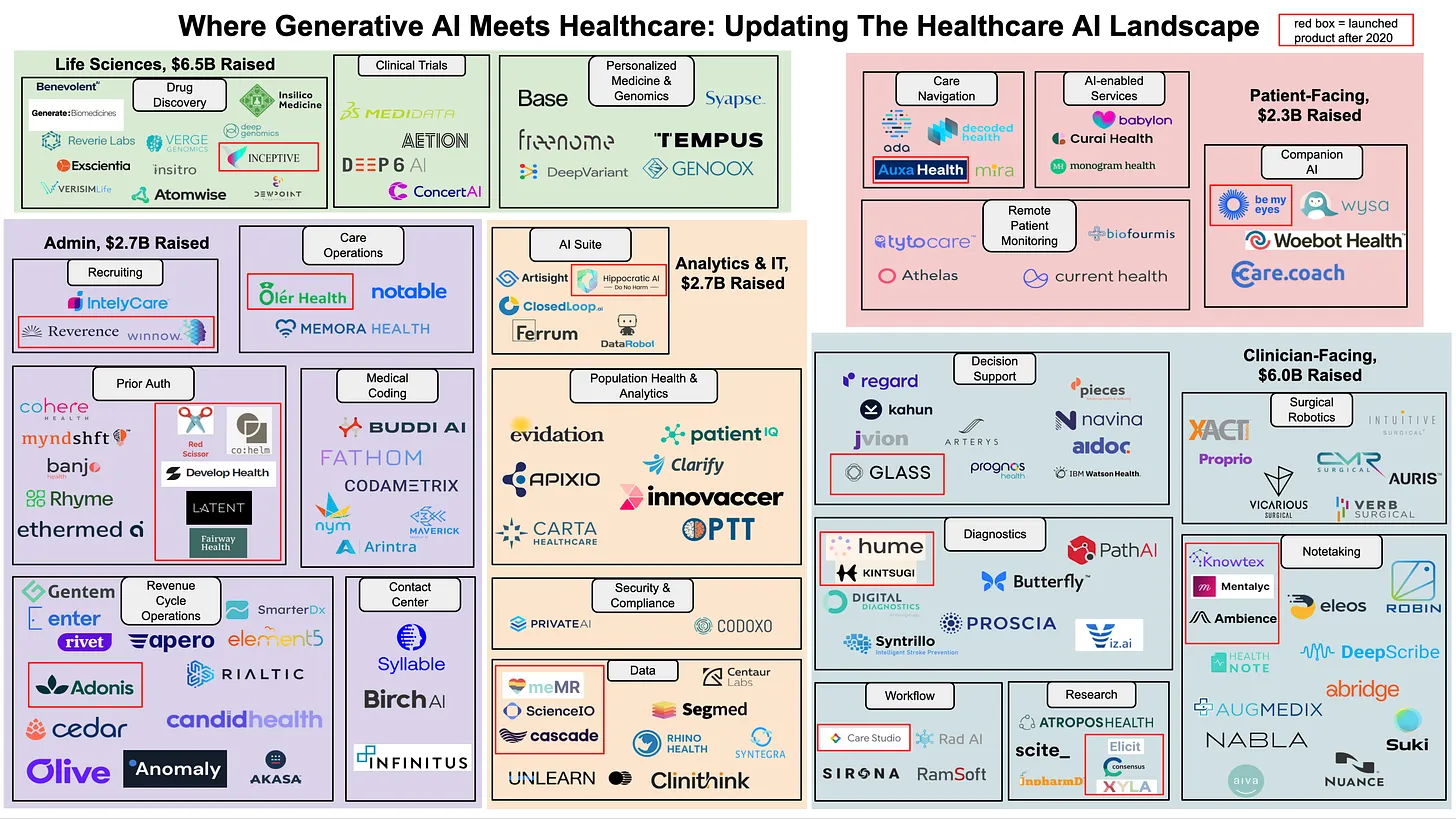

Figure 9

Gen AI is where both entrepreneurs and investors continue most focused disproportionately.

The fundamental innovation is that it allows converting unstructured to structured data in a more scalable way. As Where Generative AI Meets Healthcare: Updating The Healthcare AI Landscape argues, the new capabilities applied to healthcare are incredible and they seem to be following or perhaps surpassing Moore’s Law in how much they are evolving. You can do tasks all the way from refining texts to synthesizing data, enhancing images to streamlining transcription, far more easily than ever before.

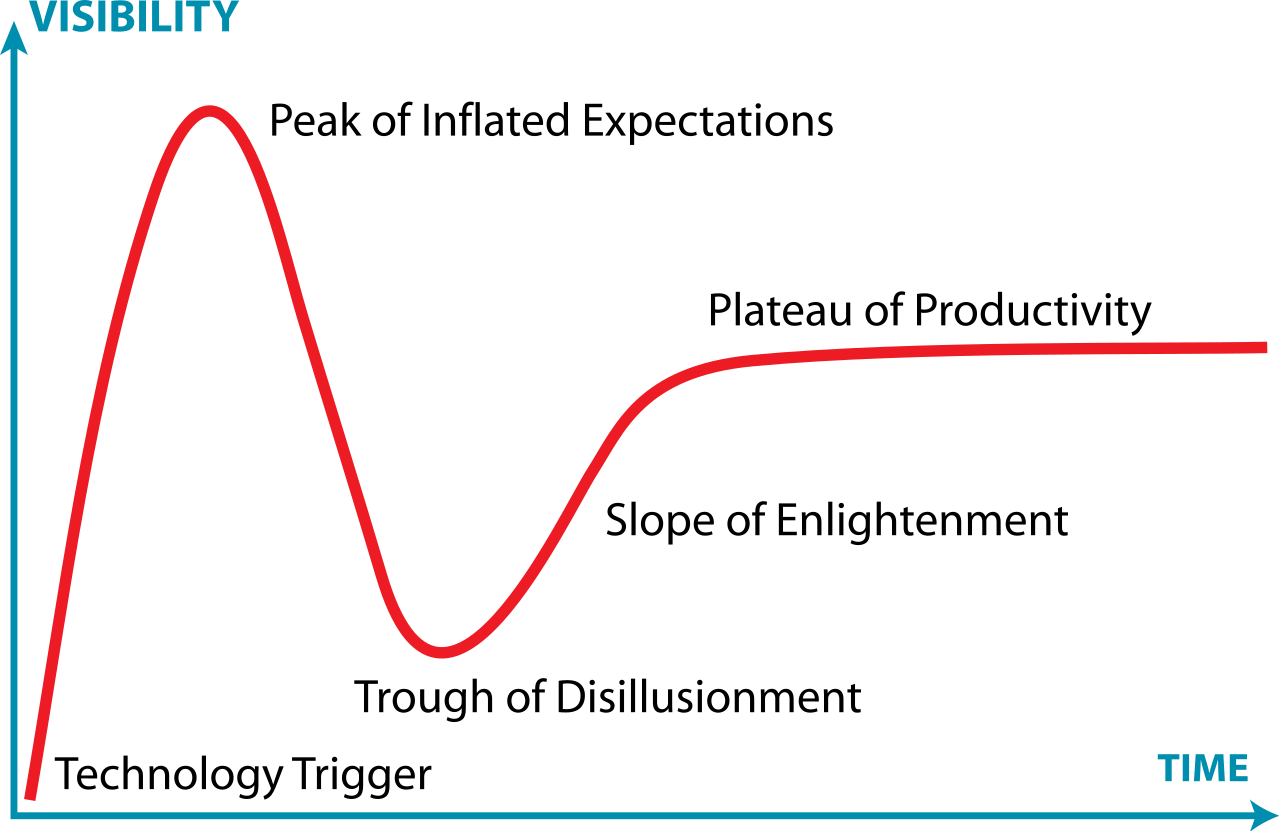

Figure 10

You may be asking whether gen AI is at the peak of inflated expectations. Or you may be looking at public comps and deciding traditional healthcare is currently in the trough of disillusionment. But the point is healthcare is a fundamental need for all of us and our current system is exacerbating this need. At the same time all the other macro factors, from funding to AI’s evolution, point to a way to building valuable companies quickly. It’s up to entrepreneurs to seize the day.

Disclaimer

Views expressed above are the author’s own.

END OF ARTICLE

[ad_2]

Source link